In my opinion investing is often represented or presented as needlessly complex. Advisors and clients alike tend to mistake complexity for effectiveness and think of simple solutions as unsophisticated and inferior to complex ones. Likewise, human nature leads us to believe in experts and reason that if there are investment experts, then one of those experts should be able to share their expertise with us and give us their same advantage

The evidence however tells another story. In the majority of instances, active fund managers underperform when compared to index investing. In the U.S., for example, 83.18% of all domestic funds underperformed their benchmark for the 10-year period ending 12/31/2015 (1). Individual investors fare even worse. According to Dalbar, in 2015, the 20-year annualized S&P 500 return was 8.19% while the 20-year annualized return for the average equity mutual fund investor was only 4.67%, a gap of 3.52% (2). This investor underperformance is called the “behavior gap” by financial advisor Carl Richards and can be attributed largely to investor behavioral biases. These self-destructive investment behavior biases include:

- Loss Aversion – The fear of loss leads to selling at the worst possible time.

- Framing – Making decisions about part of a portfolio without considering the total picture.

- Anchoring – The process of remaining focused on past events or prices.

- Mental Accounting – Separating performance of individual investments to justify success and failure.

- Herding– Following what everyone else is doing.

- Regret – Not performing a necessary action due to the regret of a previous failure.

- Overconfidence – Believing in our ability to select “winners,” despite the evidence.

In the end, we are just human. Despite the best of our intentions, it is nearly impossible for an individual to be devoid of the biases that inevitably lead to poor investment decisions over time.

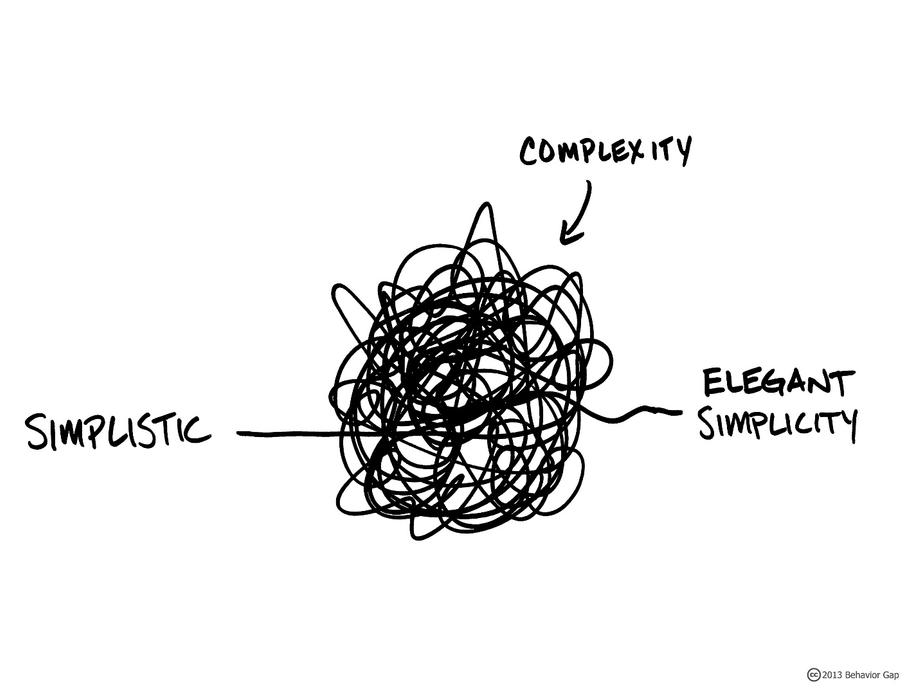

I believe investment portfolios should be designed based on the concept of “elegant simplicity.”

Portfolio design is based on a deep understanding of historical returns and seeks to maximize diversification, transparency and tax efficiency. Portfolios are constructed using Dimensional Fund Advisors whose mission is "about implementing the great ideas in finance for our clients."

[1] S&P Dow Jones Indices. SPIVA US Scorecard: Year-End 2015. McGraw Hill Financial. http://us.spindices.com/resource-center/thought-leadership/research/

(2) http://seekingalpha.com/article/3983253-dalbar-2016-yes-still-suck-investing-tips-advisors

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

The Standard & Poor’s 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

DFA and LPL Financial are separate entities.